Our complete payment processing fees comparison breaks down interchange-plus vs. flat-rate pricing to help your business find the most cost-effective provider.

When you're trying to make a payment processing fees comparison, that shiny advertised rate—something like 2.9% + $0.30—is really just the tip of the iceberg. The real cost of taking card payments is always a mix of fixed wholesale fees and the processor's own markup. That markup is where you can actually find some savings.

Every single time you accept a card payment, the fee you're charged gets split into three separate pieces. Getting a handle on these is the first real step toward making a smart choice for your martial arts school.

For years, the standard payment processing fee has hovered somewhere between 1.5% and 3.5% of the transaction. But those rates only tell you part of the story. You also have to factor in the other costs that chip away at your bottom line, like chargebacks, fraud prevention tools, and general admin overhead. These can easily tack on another 1-2% of your total sales.

To get a true picture of what you're spending, you have to know [how to effectively track business expenses](https://alliedtax.com/how to track business expenses/). That kind of clarity shows you exactly where every dollar is going.

Your goal isn't just to find the lowest rate. It's to find the most transparent and predictable pricing that eliminates surprise costs and actually fits how your school operates. For most martial arts schools, that means looking past the simple flat-rate options.

Think of this table as your cheat sheet for the main fees you'll run into. Understanding who sets them and why they exist gives you the foundation you need to compare providers intelligently.

Getting a grip on these individual costs is absolutely essential. To get a breakdown tailored for schools like yours, check out our guide on https://www.martialytics.com/blog/payment-processing-for-small-businesses-made-simple.

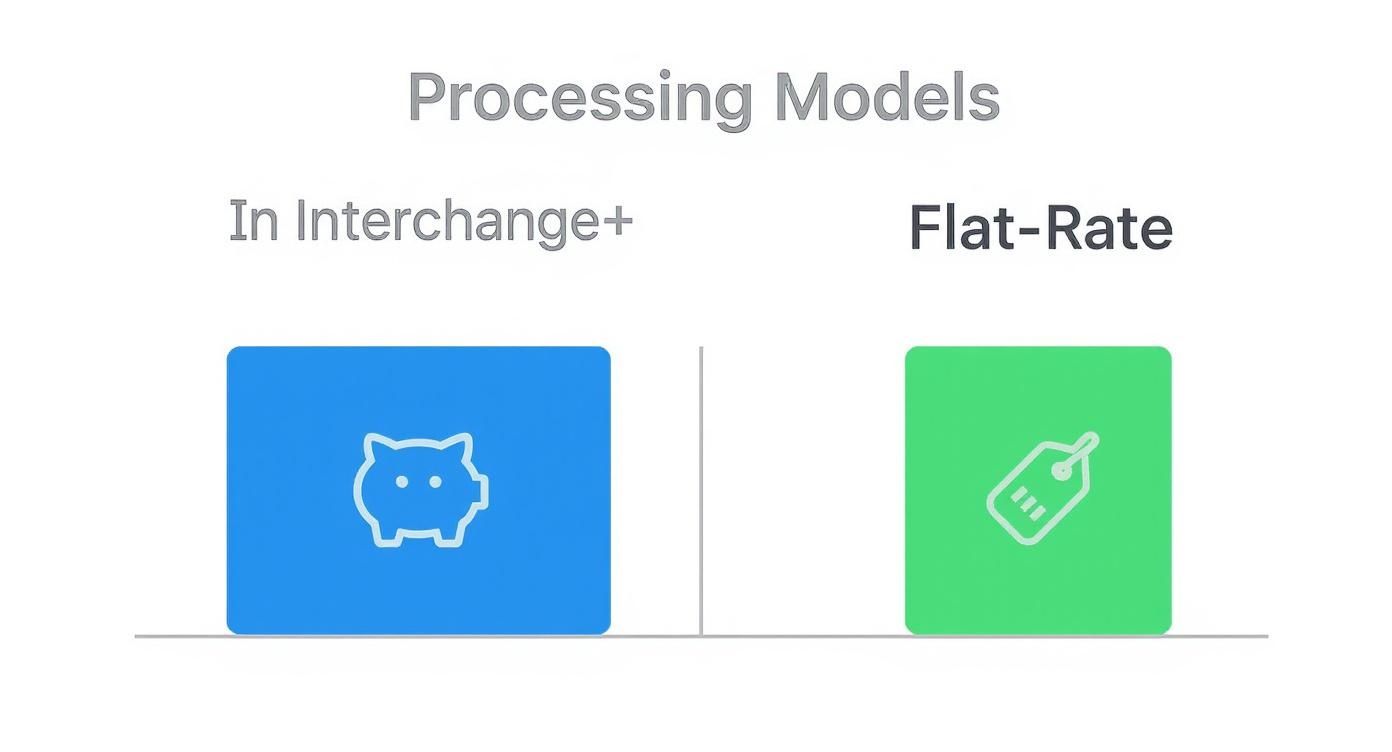

When you're picking a payment processor, it all boils down to their pricing model. The two you'll run into most often are Interchange-Plus and Flat-Rate, and the one you choose can seriously impact your school's bottom line. Let's break down how each one really works for a martial arts school.

Flat-rate pricing is all about simplicity. Companies like Stripe and Square take all the different fees—interchange, assessments, and their own markup—and roll them into a single, predictable rate, like 2.9% + $0.30. This makes it incredibly easy to guess what your processing costs will be each month.

But that simplicity often has a hidden cost. Because you’re paying the same rate for every single transaction, you end up overpaying on cheaper ones (like debit cards) to cover the higher cost of premium rewards credit cards.

For a brand new or smaller school processing under $5,000 a month, a flat-rate model is usually the best place to start. You typically won't have monthly fees, and you know exactly what you’ll pay on every transaction without having to become an expert on payment processing statements.

Let's look at a real-world example:

The processor just made a $4.10 profit on that one transaction. While that difference seems huge, the trade-off is that you're not paying monthly account fees or separate PCI compliance charges, which can make it a fair deal for schools with lower volume.

Interchange-plus, on the other hand, is built for transparency. This model doesn't bundle everything together. Instead, it separates the non-negotiable wholesale costs (the interchange and assessment fees) from the processor's markup. Your statement will clearly show the true cost of each card swiped, plus the processor's fee, which might look something like 0.40% + $0.15.

With this model, the actual cost of the card is passed directly to you. This is a huge deal, because interchange fees vary wildly. In the United States, for instance, the average interchange fee is around 1.8% for credit cards but only 0.3% for debit cards. That difference adds up fast.

Because the processor's markup is a small, fixed percentage, you get to keep the savings when students pay with lower-cost cards, like debit. This is where established schools start to see some serious money back in their pockets.

Key Takeaway: Go with Flat-Rate for its sheer simplicity and predictability, especially if your monthly processing volume is low. But once your school is processing over $5,000-$10,000 a month, it's time to switch to Interchange-Plus to take advantage of lower wholesale costs and save money.

Let’s run that same scenario again, but this time with an interchange-plus model.

That’s a massive saving compared to the $4.65 you'd pay on a flat-rate plan for the exact same transaction. As your school grows and you process more payments, those savings become even more significant. This transparency gives you a crystal-clear view of what you're actually paying for, making it much easier to manage your school's finances.

When you're looking at different options, pay attention to how they present their pricing. For an example of a straightforward approach, you can see how we structure things on our Martialytics pricing page. Understanding these two models is one of the most important steps in protecting your school's financial health.

Picking a payment processor means looking past the big, bold numbers they advertise on their homepages. To really understand what you'll be paying, you need to compare how those fees actually play out as your school grows.

Let's put two flat-rate giants, Stripe and Square, head-to-head against an interchange-plus player, Payment Depot, to see the true cost at different revenue levels. We'll dig into their effective rates, hardware costs, and software, giving you a clear picture of what works best for a martial arts school at every stage.

This chart gives a great high-level view of the two main pricing models we're about to break down.

As you can see, flat-rate is all about simplicity. You get one predictable percentage. Interchange-plus, on the other hand, separates the wholesale cost from the processor's markup, which almost always means lower fees for more established businesses.

Stripe has become a go-to for online-focused businesses, and for good reason. Its tools are powerful and it integrates with just about everything. The standard fee is a clean 2.9% + $0.30 per transaction. That predictability is fantastic when you're just starting out and need to forecast your costs easily.

But here’s the catch with that simplicity. You're paying the exact same rate for a low-cost debit card transaction as you are for a premium rewards card. For a dojo processing dozens of membership payments each month, you could be overpaying on a huge chunk of your transactions without even realizing it.

Square uses the same flat-rate model as Stripe, charging 2.9% + $0.30 for online payments. But where Square really shines for a business like a martial arts school is its point-of-sale (POS) hardware. They make it incredibly easy and affordable to take payments in person at your front desk, whether it's for a new gi or a drop-in class.

Just like Stripe, though, that convenience has its limits. As your school grows, the blended rate starts to work against you. You miss out on the savings from low-cost debit and standard credit cards, which likely make up the bulk of your membership payments.

Key Insight: The main draw for Stripe and Square is their simplicity and lack of monthly fees. This makes them the perfect starting point for a brand-new school. But their value starts to drop off once you’re consistently processing over the $5,000 to $10,000 per month mark.

Payment Depot flips the script. Instead of a percentage markup, they use an interchange-plus model paired with a monthly subscription. You pay the direct, wholesale interchange rate for every transaction, plus a tiny fixed fee (like $0.05 - $0.15). To get this direct rate, you pay a monthly membership fee, which usually starts around $79.

For any school processing over $10,000 a month, this model is almost guaranteed to save you money. Why? Because you get the full benefit of low-cost debit card transactions, and the processor’s profit is capped by that flat monthly fee—not a percentage of your hard-earned revenue.

When you're trying to figure out the best processor, you have to look at the whole picture. For schools with international students or plans, for instance, you'll also want to compare providers and fees for transferring money overseas to manage those payments effectively.

To make this comparison really hit home, let's look at how the costs stack up for a martial arts school as its revenue changes. This table breaks down what really matters.

Let’s put this into practice. For a dojo processing $5,000 a month, Stripe or Square is the obvious choice—no monthly fee makes them cheaper. But fast forward a year, and that same school is now processing $25,000 a month. Suddenly, the savings from Payment Depot's interchange-plus model will blow its monthly fee out of the water, making it the smarter financial decision.

This is the perfect example of why the best processor for your school today might not be the best one for you in two years. It's all about matching the model to your volume.

The transaction rate is what every processor wants you to focus on. It’s the shiny number they dangle in front of you. But I’ve seen countless school owners get burned by the less obvious costs that actually inflate their monthly bill.

These sneaky charges, often buried deep in the fine print of a merchant agreement, can turn a seemingly great deal into an expensive nightmare. Understanding what these fees are—and where they hide—is the first step to protecting your school’s bottom line.

Processors often use these extra fees to pad their margins, knowing that most business owners are laser-focused on that main percentage rate. But from compliance penalties to random account charges, these costs can stack up fast, sometimes jacking up your effective rate by a full percentage point or more.

One of the most common offenders I see is the PCI compliance fee. This charge, which can run anywhere from $20 to $100 a month, is for validating that your school handles cardholder data securely. While compliance itself is non-negotiable, some processors charge an arm and a leg for it or hit you with massive penalties if you miss a deadline.

On top of that, you have to watch out for a whole menu of routine account fees that serve little purpose beyond lining the processor’s pockets. These often include:

Always demand a full, itemized fee schedule before you even think about signing a contract. If a provider gets cagey or claims their “flat rate” covers everything, that’s a huge red flag. Real transparency means they aren’t afraid to show you every single potential charge, no matter how small.

Think about it this way: a school processing $8,000 a month might spend weeks negotiating a slightly lower transaction rate. But a $75 monthly PCI fee and a $20 statement fee add $95 in fixed costs out of nowhere. Those costs completely wipe out any savings you thought you got from the rate negotiation.

Processors also make a killing on punitive fees—charges triggered when something goes wrong, like a customer dispute or you trying to leave their service.

The chargeback fee is a perfect example. This is a penalty of $15 to $50 applied every time a parent or student disputes a transaction, and you get hit with it whether you win the case or not. For a martial arts school, just a few disputed membership payments could saddle you with hundreds of dollars in penalties.

But the real monster is the Early Termination Fee (ETF). If you’re locked into a multi-year contract and realize you need to switch providers, you could be on the hook for a $300 to $500 penalty. Some of the most aggressive contracts even have a "liquidated damages" clause, where the penalty is based on the processor's projected lost profits for the rest of your contract. It can be devastating.

To protect your dojo, you have to actively seek out providers that offer month-to-month agreements with no cancellation penalties. This doesn't just save you from a potential financial trap; it forces the processor to earn your business every single month. When you’re looking at a contract, find these terms first. They tell you everything you need to know about how that company views its relationship with you.

It’s one thing to read the fees on your statement, but it's another thing entirely to understand why they change. The world of payment processing isn't a bubble. Big-picture economic trends have a direct impact on the rates you pay, and getting a handle on these shifts is crucial for choosing a partner for the long haul.

Payment processors are businesses, and like any business, they’re focused on growth. But that growth is hitting a snag. From 2019 to 2024, global payments revenue grew at a healthy 7% clip each year. In 2024, that slammed down to just 4%. This slowdown is tied to bigger issues like peaked interest rates and a major consumer shift toward cheaper ways to pay. For you, this means processors are feeling the squeeze and looking for ways to protect their revenue—often by tweaking merchant fees. You can read more about these global payment trends here.

This pressure usually shows up in subtle ways. You might see a small bump in your monthly account fee, a new charge for a service that used to be free, or find that your processor is suddenly unwilling to negotiate their markup. It's a quiet but constant push to keep their profit margins up in a tougher market.

Another major trend hitting your bottom line is the explosion of alternative payment methods. Your students and their parents are getting more and more comfortable using digital wallets like Apple Pay and Google Pay, not to mention direct bank transfers (also known as ACH payments). This shift is both a challenge and a massive opportunity for your school.

While many digital wallet payments still run on the old credit card networks (and come with similar fees), the rise of ACH is a game-changer, especially for recurring membership dues.

By actively offering and even incentivizing ACH payments, you can sidestep a huge chunk of the volatile interchange fee system. It’s a proactive way to control your costs instead of just reacting when your processor decides to raise rates.

Processors are adapting. Many now highlight their "multi-rail" capabilities, giving you access to card networks, ACH, and digital wallets all in one place. The trick is to find a partner whose fee structure for these cheaper methods is genuinely cost-effective and not just a marketing gimmick.

The payment processing industry has seen a lot of buyouts, with the big fish swallowing up smaller competitors. On the one hand, this can lead to more powerful, all-in-one platforms. On the other, it shrinks the pool of competition, which means fewer options and less bargaining power for you.

When a handful of large companies dominate the market, they feel less pressure to offer aggressive pricing to win your business. This makes it absolutely critical to scrutinize your options and understand the true cost of a provider’s service, not just their flashy advertised rate.

Finding ways to automate business processes can also help offset these rising operational costs. Ultimately, staying on top of these trends helps you see changes coming and pick a payment partner that truly supports your school's financial health for years to come.

Let's be honest, the world of payment processing can feel like a maze. But a few straight answers can clear up the fog and help you make much smarter financial decisions for your martial arts school.

This isn't just about finding the lowest rate; it's about understanding the real cost of getting paid. We'll tackle the most common questions and concerns we hear from school owners every day.

Yes, you absolutely can. While the wholesale interchange rates set by card networks like Visa are non-negotiable, the processor’s markup is where you have real leverage. For most martial arts schools processing over $10,000 per month, there's almost always room to negotiate a better deal.

The trick is knowing your numbers. You have to get comfortable reading your processing statement so you can see exactly what your processor is charging on top of the base costs. Once you have that figured out, you can shop around for quotes on an interchange-plus plan and bring them back to your current provider.

Don't forget to highlight your strengths—things like consistent monthly volume, a low chargeback history, and a healthy average payment size. These are powerful bargaining chips. If your current processor won't play ball, don't be afraid to walk.

The "cheapest" way really depends on where your school is at. For a brand new dojo with just a handful of students or unpredictable sales, a flat-rate provider like Square can actually be the most affordable starting point because you avoid monthly fees.

However, once your school has consistent volume (anything over $5,000 per month), an Interchange-Plus pricing model almost always becomes the more cost-effective choice. This structure passes the true wholesale cost of each transaction directly to you, plus a small, transparent markup. You end up benefiting from the lower costs associated with debit cards and other low-risk payments.

The real secret weapon for martial arts schools? ACH payments (e-checks). They are significantly cheaper than cards. ACH fees are often a flat rate capped at just a few dollars, no matter the size of the payment. This makes it the perfect, low-cost solution for collecting those larger recurring membership dues.

Choosing the right processor means looking way beyond the advertised rate. The single most important factor is how well it integrates with your existing martial arts management software. If it can't handle critical functions like automated invoicing or recurring billing seamlessly, the cheap rate isn't worth the headache.

For most established schools, an Interchange-Plus model is the best financial fit. You should also make sure any potential partner has robust ACH processing capabilities. This is non-negotiable for cutting costs on your most frequent and largest payments—your monthly memberships.

Finally, take a hard look at their customer support and the tools they offer for managing chargebacks. Payment disputes happen, and they can become incredibly expensive and time-consuming if your processor doesn't give you the support and tools to fight them effectively.

Martialytics simplifies all of this by offering transparent, low-cost processing designed specifically for martial arts schools, including seamless ACH integration. Start your 30-day free trial today and see how much you could actually be saving.

No credit card required. No lock in contracts. Start your 30-day free trial to see immediate improvements.

Book your free demo with one of the co-founders of Martialytics, Brad or Allen, depending on your time-zone.

We'll do this on Zoom video conferencing software for awesome screen sharing so please make sure you have the app or are good to go before the time starts.

The easiest to use Martial Arts School Management Software in the world.