Unlock growth with our guide to payment processing for small businesses. Learn to choose the right tools, cut fees, and streamline your operations.

Payment processing is simply the collection of tools and services that let you accept credit cards, debit cards, and other digital payments from your customers. Think of it as the essential financial plumbing that moves money securely from their bank account to yours, making sure you get paid.

Let’s be honest—the world of payment processing can feel like a tangled mess. But what if you stopped seeing it as just another business cost and started seeing it as the central nervous system for your cash flow? This shift in perspective changes everything. It turns a confusing technical hurdle into a powerful tool for growth.

Think of your payment processor as a trusted financial translator. When a student or their parent pays, the processor ensures their bank and your bank can speak the same language, securely and almost instantly. It’s the behind-the-scenes magic that makes modern business possible.

Every time a card is swiped, tapped, or entered online, a lightning-fast and secure conversation happens between a few key players. Understanding who they are demystifies the whole thing.

For small businesses, slow payments and high fees aren't just a headache; they're a direct threat to survival. Efficient payment processing for small businesses frees up cash, slashes admin time, and lets you focus on what you actually love doing—running your business.

Choosing the right partner for this is more than a technical decision; it's a strategic one. A smooth payment experience builds trust with your customers, while a clunky one can lead to lost sales and frustration. The right system also provides rock-solid security to protect sensitive data, which is non-negotiable today.

By exploring the benefits of streamlined business management, you can see how integrated payments are a huge piece of the puzzle for a healthy operation. Ultimately, a smart payment solution is a cornerstone of your financial stability and long-term success.

Ever wondered what really happens in those few seconds between a card swipe and the ‘Approved’ message? It feels instant, but there’s a complex, high-speed journey taking place behind the scenes.

This is the story of a single payment, following its path from your customer's wallet all the way to your business bank account.

Let's break down this digital relay race into three main stages: authorization, clearing, and settlement. Each step involves different players working together to make sure the money moves safely and ends up exactly where it should.

The moment your customer taps their card, the race begins. Your point-of-sale (POS) terminal or online checkout page captures the card information, encrypts it, and sends it through a payment gateway. Think of the gateway as a secure messenger that delivers the transaction details to your payment processor.

The processor then contacts the customer's bank (the issuing bank) to ask a simple, critical question: "Does this person have enough funds or credit for this purchase?"

In a split second, the bank checks the account and sends back a "yes" or "no." This approval or denial travels all the way back through the same channels, finally popping up on your screen. This entire back-and-forth usually happens in just one to two seconds.

Once the day is done, all those authorized transactions are bundled together into a batch. Your processor sends this batch to the card networks (like Visa or Mastercard). This is the clearing phase, where everyone double-checks that the details are correct.

Finally, we get to settlement—the part where the money actually moves. The card networks tell the customer's bank to transfer the funds to your business bank account (the acquiring bank). This process used to take days, but modern systems have cut that time down dramatically.

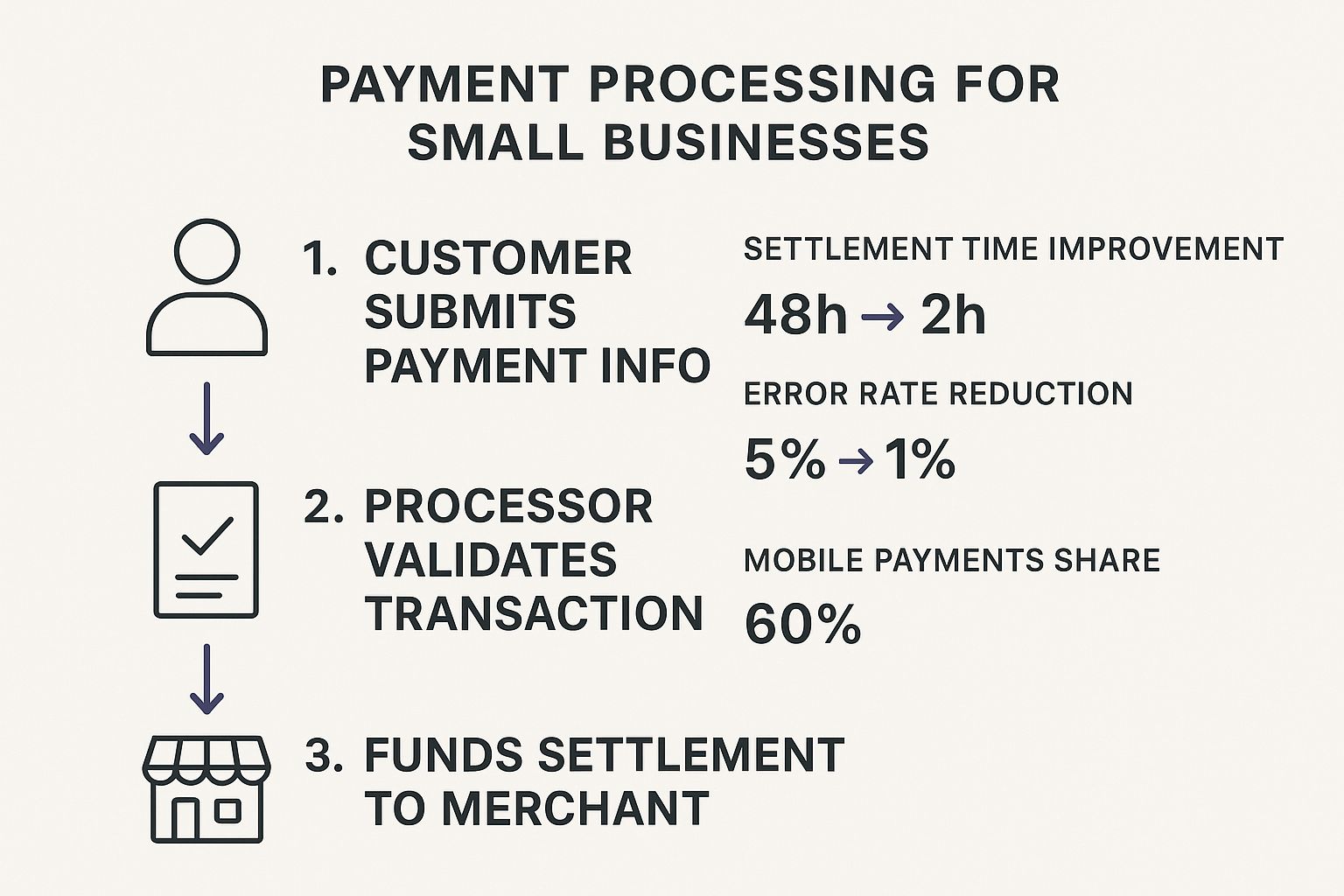

This infographic really brings to life how much faster and more reliable this whole workflow has become for small businesses.

As the visual shows, we're seeing settlement times shrink from days to hours, and error rates are plummeting. The massive growth in mobile payments also highlights a huge shift in how customers want to pay.

This move toward digital isn't just a trend; it's the new standard. Over 70% of global consumers now use digital payments, a major shift away from cash that started during the pandemic and is clearly here to stay. You can find more great insights on this shift over at PayCompass.com.

Understanding this journey from start to finish gives you the confidence to manage your cash flow, because you know exactly how and when you’ll get paid.

Picking a partner for your payment processing for small businesses is a much bigger deal than just a technical setup. Think of it as a critical financial partnership. The right processor works quietly in the background, keeping your cash flow steady and predictable.

But the wrong one? That’s a recipe for hidden fees, long waits on support calls, and a whole lot of operational headaches.

The first step to making a smart choice is to look past the flashy, low transaction fee. You’ve got to see the whole picture: the pricing models, the fine print in the contract, their security standards, and what happens when you actually need to call customer support. This is how you find a partner that truly fits your business, not just today, but wherever you plan to grow.

How a processor charges you directly chips away at your bottom line. You’ll mostly run into two main ways they structure their fees: flat-rate and interchange-plus. Each has its place, depending on your sales volume and how you run your business.

The global digital payment market is massive, hitting around $122.32 billion in 2024. A huge chunk of that growth is coming from small businesses jumping on board with easy-to-use platforms like Square, Stripe, and PayPal. These guys often use that simple flat-rate model, making it easier than ever for anyone to start accepting digital payments.

To help you get a clearer picture, here’s a quick comparison of some of the top payment solutions. This table breaks down their features and pricing so you can make a more informed decision about what works for your small business.

Remember, the "best" processor is relative. What’s perfect for a coffee shop with tons of small, in-person sales might not be the best fit for an online retailer with larger, less frequent transactions. Use this as a starting point for your own research.

While cost is always a big piece of the puzzle, it’s definitely not the only one. A truly great payment partner brings more to the table than just a low rate.

A critical factor in choosing the right payment partner is ensuring they adhere to robust data security measures to protect both your business and your customers.

Let's be clear: your processor is handling incredibly sensitive financial data every single day. Security isn't just a feature; it's a must-have. Make sure any partner you consider is fully PCI compliant, which is the industry-wide standard for protecting cardholder data. Failing to meet these standards can lead to massive fines and, even worse, a complete loss of your customers' trust.

Next, read the contract. I mean, really read it. Steer clear of partners that try to lock you into long, inflexible contracts with huge fees if you want to leave early. A provider that’s confident in their service will earn your business month after month, not force you to stay.

And finally, give their customer support a test run. When a payment fails on your busiest day, you need a helpful human on the other end of the line, not a robot sending you in circles.

This is where integrated solutions can be a lifesaver. Software built for your specific industry often has payment processing baked right in, which saves you from the headache of juggling multiple systems. You can see exactly how an all-in-one system smooths everything out by requesting a Martialytics demo.

In the past, payment processing was just about getting money from Point A to Point B. Today, that’s just the starting line. Think of your payment system less like a cash register and more like your business's central nervous system—a hub of smart tools designed to help you work smarter, not harder.

When your payment solution starts doing the heavy lifting for you, it stops being a simple expense and becomes your most valuable employee. The right features automate the grunt work, reveal powerful insights, and give you back your most precious resource: time.

For most small business owners, chasing down late payments and manually creating invoices is a soul-crushing time sink. This is where features like automated recurring billing and integrated invoicing aren't just nice—they're necessary. They put your revenue on autopilot and claw back hours of your week.

For any business built on regular payments, using efficient recurring payment solutions for modern businesses is a total game-changer. It stabilizes your income so you can stop being a bill collector and get back to serving your clients.

Every transaction you process tells a story. Modern payment processors come packed with reporting and analytics tools that turn your raw sales numbers into a clear roadmap for growth. It’s time to stop guessing what works and start making decisions based on real data.

A local bakery might use its sales reports to discover that croissants outsell muffins 3-to-1 on Saturday mornings, helping them nail down their baking schedule and slash waste. In the same way, a martial arts school can track enrollment trends to see when to add a new kids' class.

These insights can show you your busiest days, your most popular services, and even your top-spending customers. This is pure gold for everything from planning your marketing to managing your inventory.

Beyond just billing and reports, the best payment systems are full of practical tools that solve real-world business problems. These are the thoughtful features that smooth out your daily workflow and make your customers’ lives easier.

A freelance consultant, for example, can use a virtual terminal to securely type in credit card details from a client over the phone. A retail shop can use a processor that offers inventory syncing, which automatically updates stock levels after every sale so they never accidentally sell an item they don't have.

It's these small, smart tools that handle the critical details, keeping your business running like a well-oiled machine.

Diving into the world of payment processing for small businesses can feel like walking through a minefield. You're trying to find a partner to streamline your cash flow, but the wrong one can slowly bleed your profits with a dozen tiny cuts you never saw coming.

The most common trap? Overly complicated fee structures. Many providers bury extra costs deep in the fine print of their merchant agreements. What starts as a great deal can quickly turn into a financial headache. Protecting your business means learning to spot these red flags from a mile away.

Your monthly statement is ground zero for hunting down hidden costs. It’s easy to focus on the main transaction percentage, but the real damage often comes from a variety of other charges that nickel-and-dime you. Getting a handle on what these are is the first step toward avoiding them completely.

Keep an eye out for these common culprits:

A truly transparent partner will have clear, straightforward pricing. Platforms like Martialytics build payment processing right in, with simple, predictable rates you can actually plan for. You can see exactly what that looks like on our clear and simple pricing structure.

A chargeback is what happens when a customer disputes a transaction with their bank, which then forcibly reverses the payment from your account. While they’re designed to protect consumers from fraud, they can become a massive headache for small businesses, costing you both the sale and an additional penalty fee.

For a small business, slow payments and high fees aren't just an inconvenience—they are a direct threat to survival. According to the U.S. Small Business Administration, a staggering 82% of businesses that fail do so because of cash flow problems. Unexpected fees and chargebacks only make that problem worse.

To keep your revenue safe, you need a clear process for handling these disputes. That means responding immediately with detailed evidence—think signed receipts, delivery confirmations, and any emails you have with the customer.

But the best defense is always a good offense. Prevention is key. Clear communication, excellent customer service, and a simple return policy can stop most disputes before they even start. By getting ahead of these challenges, you’ll protect your profits and build a much healthier financial foundation for your business.

Even after you get the basics down, the world of payment processing for small businesses can leave you with some nagging questions. Let's tackle the most common ones head-on, with clear, straightforward answers to help you navigate your options with confidence.

Think of this as your quick-reference guide for the topics that often cause the most confusion.

It’s easy to get these two terms mixed up because they’re partners in every single transaction. The simplest way to think about it is to picture a secure digital messenger and a bank.

Modern, all-in-one solutions like Stripe or Square bundle both services together, which is why the line has blurred. They provide the gateway and the processing, creating one seamless experience for you.

Not always, and this is a huge difference between payment providers today. A merchant account is a special type of bank account that allows a business to accept and hold funds from credit or debit card transactions before they land in your regular business account.

Traditional providers require you to apply for your own dedicated merchant account, which can be a slow, paperwork-heavy process.

But modern payment service providers (PSPs) like PayPal and Square work differently. They're what's known as "aggregators," meaning you operate under their master merchant account. This makes setup incredibly fast and easy for a small business, though it can sometimes lead to stricter holds on funds if your activity is flagged as unusual.

Reducing fees is one of the fastest ways to improve your profit margins. While some costs are fixed, you have more control than you might think. Here are a few practical strategies you can implement right away:

The inability to access funds quickly can create a ripple effect, impacting everything from inventory management to hiring decisions. Faster, cheaper payments simplify how you manage cash flow and empower you to grow your business more aggressively.

The Payment Card Industry Data Security Standard (PCI DSS) is a set of mandatory security rules for any organization that accepts, processes, stores, or transmits credit card information. Its entire purpose is to maintain a secure environment and shield sensitive data from breaches.

Being PCI compliant isn't just a good idea—it's essential. Failing to comply can lead to severe fines, legal trouble, and a complete loss of your customers' trust, which is often impossible to win back.

The good news is that most reputable payment processors build compliance tools directly into their platforms. They help you meet the requirements automatically and keep your business, and your customers, safe.

Stop wasting time chasing payments and start focusing on your students. Martialytics integrates simple, secure payment processing right into your school management software, automating your billing so you can get back to the mat. See how it works by visiting us at https://martialytics.com.

No credit card required. No lock in contracts. Start your 30-day free trial to see immediate improvements.

Book your free demo with one of the co-founders of Martialytics, Brad or Allen, depending on your time-zone.

We'll do this on Zoom video conferencing software for awesome screen sharing so please make sure you have the app or are good to go before the time starts.

The easiest to use Martial Arts School Management Software in the world.